If you desire a house that's priced above your local limitation, you can still receive a conforming loan if you have a big enough down payment to bring the loan quantity down below the limit. You can reduce the rates of interest on your mortgage by paying an up-front charge, called mortgage points, which consequently decrease your month-to-month payment. what is the maximum debt-to-income ratio permitted for conventional qualified mortgages.

In this method, buying points is said to be "buying down the rate." Points can likewise be tax-deductible if the purchase is for your main residence. If you plan on living in your next home for at least a decade, then points might be an excellent alternative for you. Paying points will cost you more than simply initially paying a higher rates of interest on the loan if you plan to sell the property within just the next few years.

Your GFE likewise consists of a quote of the overall you can expect to pay when you close on Great site your home. A GFE assists you compare loan offers from different lending institutions; it's not a binding contract, so if you decide to decrease the loan, you will not need to pay any of the fees noted.

The rates of interest that you are priced estimate at the time of your mortgage application can change by the time you sign your mortgage. If you wish to prevent any surprises, you can spend for a rate lock, which devotes the loan provider to providing you the initial rate of interest. This assurance of a set rate of interest on a mortgage is only possible if a loan is closed in a defined time period, typically 30 to 60 days.

Rate locks can be found in numerous types a portion of your home loan amount, a flat one-time fee, or just a quantity figured into your rate of interest. You can secure a rate when you see one you desire when you initially get the loan or later while doing so. While rate locks generally avoid your interest rate from increasing, they can likewise keep it from going down.

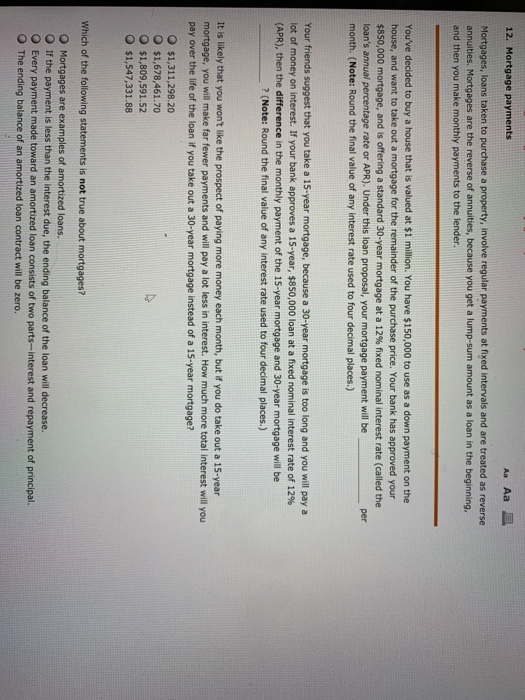

How Do Reverse Mortgages Work In Utah Can Be Fun For Anyone

A rate lock is worthwhile if an unexpected boost in the interest rate will put your home loan out of reach. what metal is used to pay off mortgages during a reset. If your deposit on the purchase of a home is less than 20 percent, then a lending institution might need you to spend for private home loan insurance coverage, or PMI, because it is accepting a lower amount of up-front money toward the purchase.

The cost of PMI is based on the timeshare experts size of the loan you are obtaining, your down payment and your credit report. For instance, if you put down 5 percent to acquire a house, PMI might cover the extra 15 percent. after my second mortgages 6 month grace period then what. If you stop making payments on your loan, the PMI activates the policy payout along with foreclosure proceedings, so that the loan provider can repossess the home and offer it in an attempt to gain back the balance of what is owed.

Your PMI can also end if you reach the midpoint of your payoff for example, if you secure a 30-year loan and you complete 15 years of payments.

Just as houses been available in various styles and price ranges, so do the ways you can fund them. While it may be simple to inform if you choose a rambler to a split-level or a craftsman to a colonial, determining what type of mortgage works best for you needs a bit more research study.

When picking a loan type, among the primary factors to think about is the kind of rate of interest you are comfortable with: fixed or adjustable. Here's a look at each of these loan types, with pros and cons to think about. This is the traditional workhorse mortgage. It earns money off over a set quantity of time (10, 15, 20 or 30 years) at a specific rate of interest.

3 Easy Facts About Hedge Funds Who Buy Residential Mortgages Explained

Market rates may fluctuate, but your rate of interest won't budge. Why would you desire a fixed-rate loan? One word: security. You won't have to fret about a rising rate of interest. Your monthly payments may change a bit with real estate tax and insurance coverage rates, but they'll be fairly stable.

The shorter the loan term, the lower the rates of interest. For instance, a 15-year repaired will have a lower rate of interest than a 30-year repaired. Why wouldn't you want a set rate? If you prepare on relocating five or perhaps ten years, you may be better off with a lower adjustable rate.

You'll get a lower initial interest rate compared to a fixed-rate home mortgage but it won't always stay there. The rates of interest changes with an indexed rate plus a set margin. However do not stress you will not be faced with big regular monthly variations. Adjustment intervals are predetermined and there are minimum and optimal rate caps to restrict the size of the change.

If you aren't planning on remaining in your home for long, or if you plan to re-finance in the near term, an ARM is something you need to think about. You can get approved for a greater loan amount with an ARM (due to the lower initial rate of interest). get more info Annual ARMs have actually traditionally surpassed set rate loans.

Rates might increase after the change period. If you don't think you'll save enough upfront to offset the future rate increase, or if you do not wish to risk needing to refinance, hesitate. What should I try to find? Look carefully at the frequency of adjustments. You'll get a lower beginning rate with more regular modifications however also more uncertainty.

The Single Strategy To Use For Which Mortgages Have The Hifhest Right To Payment'

Counting on a refinance to bail you out is a big threat. Here are the types of ARMs offered: Your rates of interest is set for 3 years then changes annually for 27 years. Your rate of interest is set for 5 years then adjusts every year for 25 years. Your rates of interest is set for 7 years then adjusts each year for 23 years.

You'll also desire to think about whether you desire or receive a government-backed loan. Any loan that's not backed by the government is called a conventional loan. Here's a take a look at the loan types backed by the federal government. FHA loans are home mortgages insured by the Federal Housing Administration. These loans are developed for customers who can't create a large down payment or have less-than-perfect credit, that makes it a popular choice for novice home buyers.

A credit rating as low as 500 might be accepted with 10 percent down. You can search for FHA loans on Zillow. Because of the costs connected with FHA loans, you might be much better off with a conventional loan, if you can receive it. The FHA requires an upfront home mortgage insurance premium (MIP) along with an annual mortgage insurance coverage premium paid monthly.

Conventional loans, on the other hand, do not have the upfront fee, and the personal home mortgage insurance coverage (PMI) needed for loans with less than 20 percent down instantly falls off the loan when your loan-to-value reaches 78 percent. This is a zero-down loan offered to qualifying veterans, active military and military households.