Table of ContentsExcitement About Which Of The Following Statements Is Not True About Mortgages?8 Simple Techniques For How Many Mortgages Should I Apply ForThe Of How Are Mortgages Calculated

The home loan, itself, is a lien (a legal claim) on the house or residential or commercial property that protects the promise to pay the financial obligation. This is what makes home loans a safe kind of debt. Because the loan is secured, effectively using the home as security, this implies that if you fall back in your payments or fail to pay the loan back, the loan provider can reclaim the home through foreclosure.

The principal is the original quantity obtained from the lending institution - what are reverse mortgages. When you protect a home loan, the lender will designate a rates of interest based on https://www.evernote.com/shard/s532/sh/670d9e64-3107-575b-53c4-7411815f856a/61da70cd8d3c624aea4b214a1ab2577c the type of home loan you choose and your credit scores. This rate figures out how fast interest builds on your home mortgage. The loan-to-value ratio is the amount of money you obtain compared to the cost or appraised value of the home you are purchasing.

For example, with a 95% LTV loan on a house priced at $50,000, you might borrow as much as $47,500 (95% of $50,000), so you would require to offer $2,500 as a deposit. The LTV ratio reflects the quantity of equity customers have in their homes. The greater the LTV ratio, the less cash property buyers are required to pay of their own funds.

The biggest difference in home loan lending pertains to the interest applied to the loan. Since you'll pay numerous countless dollars in interest over the life of even a typical mortgage, it's necessary to get the rate of interest that's right for your monetary situation. The right interest rate can help you conserve money over the life of the loan and prevent monetary distress.

Your housing costs are unaffected by market conditions. Adjustable Rate Mortgages (ARMs) Rates of interest modifications on a routine schedule (generally every 1, 7, or 10 years) 30 yearsYou can certify with lower credit. When rates of interest are low, you will pay less money. However, if rate of interest increase, you will be needed to pay more cash.

Balloon MortgageLow rates of interest over an introductory period5 years, 7 years, or 10 yearsYou have low payments (in many cases, interest just) for a set period, then the complete balance is due or the loan must be refinanced. Most of the times a fixed rate home loan is typically the better choice, due to the fact that you know exactly what you will require to pay each month, there will not be any surprises down the road, and you aren't at the mercy of market conditions.

If the rate is high when your interest rate adjusts, your payments will increase. An ARM may make sense if you are positive that your income will increase steadily for many years or if you expect a move in the future and aren't worried about potential increases in interest rates.

Facts About What Is The Current Interest Rate For Home Mortgages Uncovered

The "term" of your home loan figures out how fast you settle the loan with interest included. So, if you have a 30-year set rate home loan, it will take 30 years to pay off your loan. If you have a 15-year loan, you will own your home in half the time it handles the 30-year mortgage.

If you have a 30-year fixed rate mortgage, for the very first 23 years of the loan, more interest will be settled than principal; this suggests larger tax deductions for those 23 years. In addition, home loan payments will take up a lower portion of your income throughout the years, since as inflation increases your expenses of living, your mortgage payments remain consistent.

In addition, equity is built faster because early payments pay off more of the principal. There are home mortgage options now offered that just need a deposit of 5% or less of the purchase rate. Nevertheless, the larger the down payment, the less cash you need to borrow and the more equity you'll have.

When thinking about the size of your down payment, consider that you'll also require money for closing costs, moving expenses, and any repair or renovation expenses. An escrow account is developed by your lending institution to reserve a portion of your regular monthly mortgage payment to cover annual charges for house owner's insurance coverage, home loan insurance (if relevant) and real estate tax.

Escrow accounts are an excellent idea since they guarantee money will always be offered for these payments. If you use an escrow account to pay property tax or property owner's insurance coverage, make sure you are not penalized for late payments, since it is the lending institution's obligation to make those payments. Down payments can be a big difficulty to house ownership.

These programs can assist you pay just 3% down as a novice home purchaser. HUD and the FHA have support programs, therefore do individual states. Need to browse for deposit help programs in the area you are seeking to purchase a brand-new home? We suggest DownPaymentResource.com.

Talk with a HUD-certified real estate counselor today to set a course so you can end up being mortgage-ready. Your monthly home mortgage payment primarily settles the principal and interest. However, the majority of lending institutions likewise consist of regional property tax, homeowner's insurance and home loan insurance coverage (if applicable). This is why monthly mortgage payments are sometimes described as PITI (principal + interest + taxes + insurance). The amount of your deposit, the size of the home mortgage loan, the rate of interest, and the length of the payment term and payment schedule will all impact the size of your home loan payment.

The Main Principles Of Reverse Mortgages How Do They Work

Interest rates can change as you buy a loan, so ask lenders if they offer a rate "lock-in" that will ensure a specific rates of interest for a specific time period; this permits you to look for home loans effectively. Bear in mind that a lending institution should divulge the Annual Percentage Rate (APR) of a loan to you.

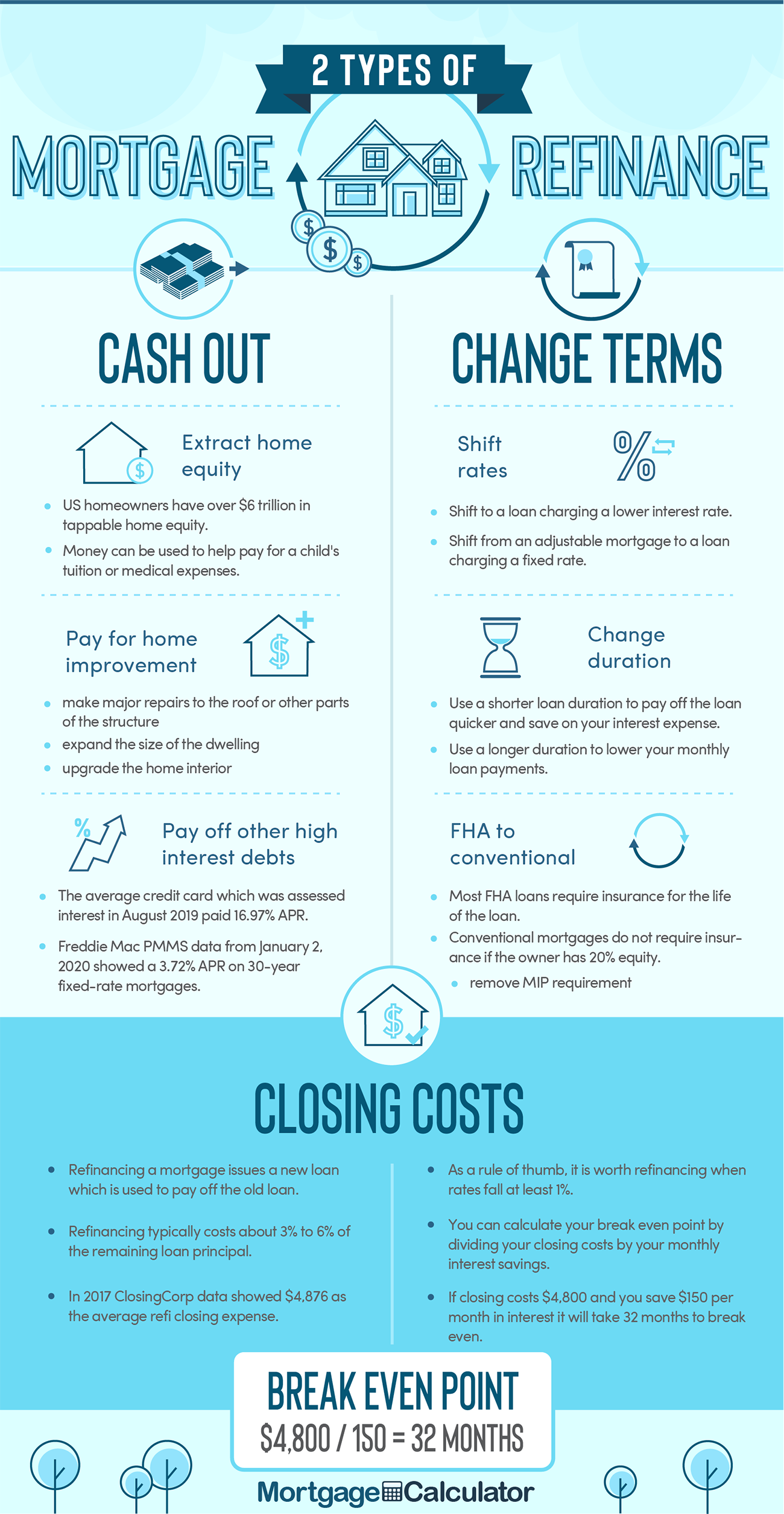

It is generally greater than the rates of interest due to the fact that it likewise consists of the expense of points, home loan insurance, and other charges consisted of in the loan. If you have a fixed-rate mortgage and rate of interest drop substantially, you may want to consider refinancing. A lot of experts agree that if you plan to be in your house for a minimum of 18 months and you can get a rate of 2% less than your present rate, refinancing is a wise choice.

Discount rate points enable you to decrease your rate of interest this is what individuals mean when they state they paid points off their mortgage. These points are basically pre-paid interest, with each point equaling 1% of the overall loan quantity. Typically, for each point paid on a 30-year home mortgage, the rates of interest is lowered by 1/8 (or.

So if you have a $200,000 home mortgage at 4.5% interest, then you could lower your rate of interest to 4.375% by paying $2,000. When looking for loans ask loan providers for a rates of interest with 0 points and after that Get more information see how much the rate decreases with each point paid. Discount points are clever if you plan to remain in a house for some time since they can decrease your monthly loan payment.

You can pay off your home mortgage faster by making additional payments every month or each year beyond your regular monthly payment requirement. This accelerates the process of settling the loan. When you send additional money, make sure to indicate that the excess payment is to be applied to the principal.